The internet began as a network of open protocols. TCP/IP let computers talk to each other, HTTP made websites possible, and IMAP, SMTP, and POP3 powered email. These were public, permissionless standards: anyone could build on them, and together they enabled global information exchange on an unprecedented scale. But they had no built-in way to capture or distribute economic value. As a result, most of the value didn’t accrue to the protocols themselves and went to centralized companies like Google, Facebook, and Amazon, which built user-facing applications and monetized attention, data, and infrastructure.

To understand why this matters, consider email. Because your inbox is portable (the underlying protocol is open) any new application can tap into the same user base instantly. There’s no re-signup friction, no need to rebuild a network from scratch. Gmail and Outlook built a massive business on top of this open layer, and Superhuman later built a premium $30/month experience on top. This ability for one layer to seamlessly build on another is called composability, and it turns out to be one of the most powerful properties of open systems. It is also native to anything built on blockchains.

These firms wrapped business models around open protocols, but the protocols themselves stayed economically passive: useful to everyone, owned by no one. Blockchains change this fundamentally by introducing programmable money, ownership, and logic directly into the protocol layer, which is why we use the name “protocol businesses”. For the first time, protocols are no longer just a technical foundation but are self-sustaining systems that can collect revenue, govern themselves, and incentivize contributors, all encoded in software. We have gone from passive internet protocols to active protocol businesses. Imagine if the three main email protocols charged a fee each time someone sends or receives an email, and imagine if you could own a piece of these protocols.

So if blockchains allow business logic to be programmed and trust to be outsourced to code, what does a protocol business actually look like? In many ways, it upends traditional assumptions about how companies operate, grow, and create value. A protocol business leverages smart contracts to automate much of its operations, and tokens (a digital representation of ownership) to incentivize and align its participants. To make this concrete, let’s walk through the key dimensions of this new model and see how it compares to what we know from the traditional world.

Traditional companies vs. protocol businesses

Core business functions

In a traditional company, core activities are handled through a combination of IT systems and human operations. A bank’s lending business, for example, involves loan officers, compliance teams, credit committees, and significant paperwork, each step adding cost and time to every transaction.

Protocol businesses automate these functions through smart contracts. Take Aave, the world’s largest decentralized lending platform: its entire lending operation runs onchain. When a borrower meets the preset conditions, loans are disbursed automatically: no loan officer, no approval queue, no paperwork. The matching of lenders and borrowers, the risk management, the fee handling, and even the liquidation of undercollateralized positions all happen through code, executing around the clock without human intervention.

What makes this particularly striking is the operational leanness it enables. Because the core business logic lives in smart contracts, these platforms can scale to handle billions of dollars in activity without expanding headcount or building out physical infrastructure. This is a fundamentally different cost structure from anything in traditional financial services.

Go-to-market & distribution

Traditional companies rely on structured go-to-market strategies to grow: sales teams, tiered pricing, paid customer acquisition, and long-term contracts designed to lock in customers and create switching costs.

Protocol businesses take a very different path. Because they launch as globally accessible networks from day one, anyone with an internet connection can start using them immediately. There’s no geographic rollout, no enterprise sales cycle, no waiting list. Adoption is often accelerated by token incentives that turn early users into financially aligned participants, creating a powerful feedback loop: the more people use the protocol, the more valuable it becomes for everyone. Growth is further amplified by crypto-native communities that serve as both distribution channels and active contributors to the product itself. This model enables remarkably capital-efficient growth with strong network effects, though it also introduces new dynamics. Loyalty can be incentive-driven rather than product-driven, and decentralized governance can sometimes slow the kind of rapid decision-making that traditional startups rely on.

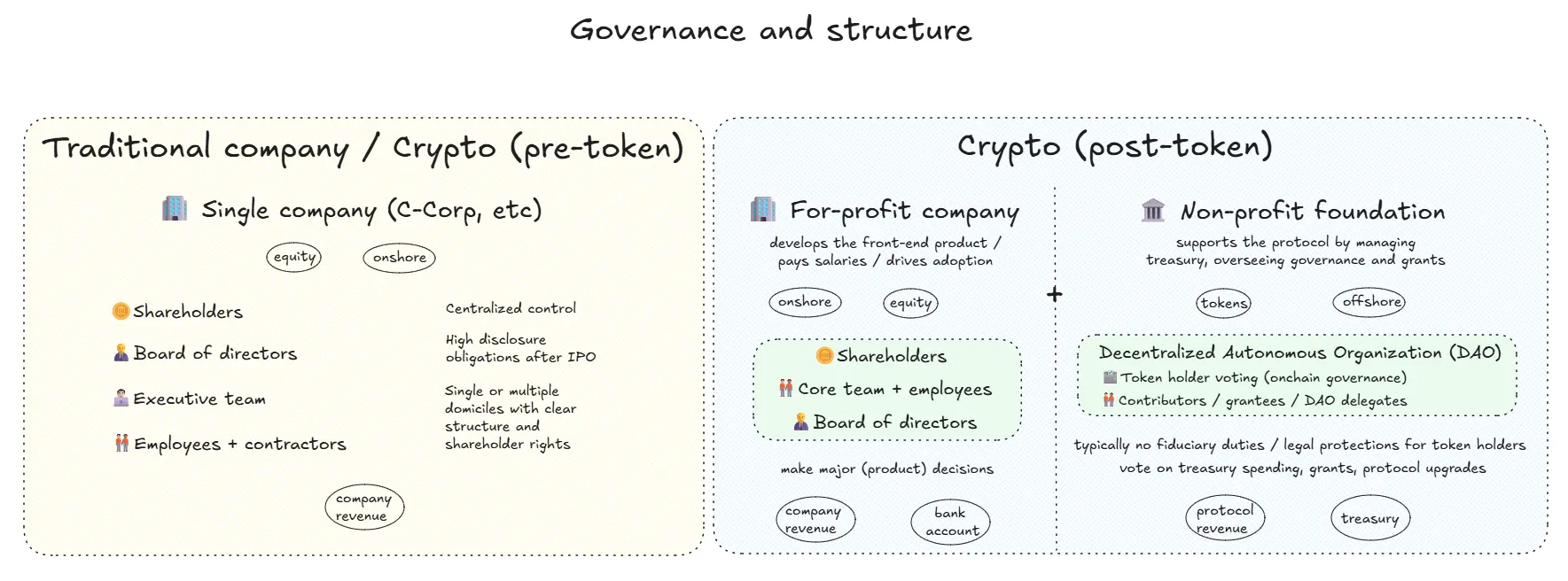

Governance & structure

Traditional companies are governed by boards of directors and executive teams, with control and decision-making flowing through a clear corporate hierarchy.

Protocol businesses typically start out looking much the same: a founding team, a company, a product roadmap. But once a token launches, a dual structure often emerges. On one side, a for-profit company continues to develop the product, manage hiring, and drive adoption. On the other, a non-profit foundation holds the token treasury, oversees governance, and manages grants to the broader ecosystem. Over time, decision-making transitions to Decentralized Autonomous Organizations (DAOs), where token holders vote on protocol upgrades, treasury spending, and key economic parameters. This is a genuinely novel form of organizational design, though it comes with its own complexities: while governance aims for broad decentralization, early investors and insiders may retain significant influence, and coordinating a global, anonymous set of stakeholders introduces challenges that traditional corporate governance simply doesn’t face.

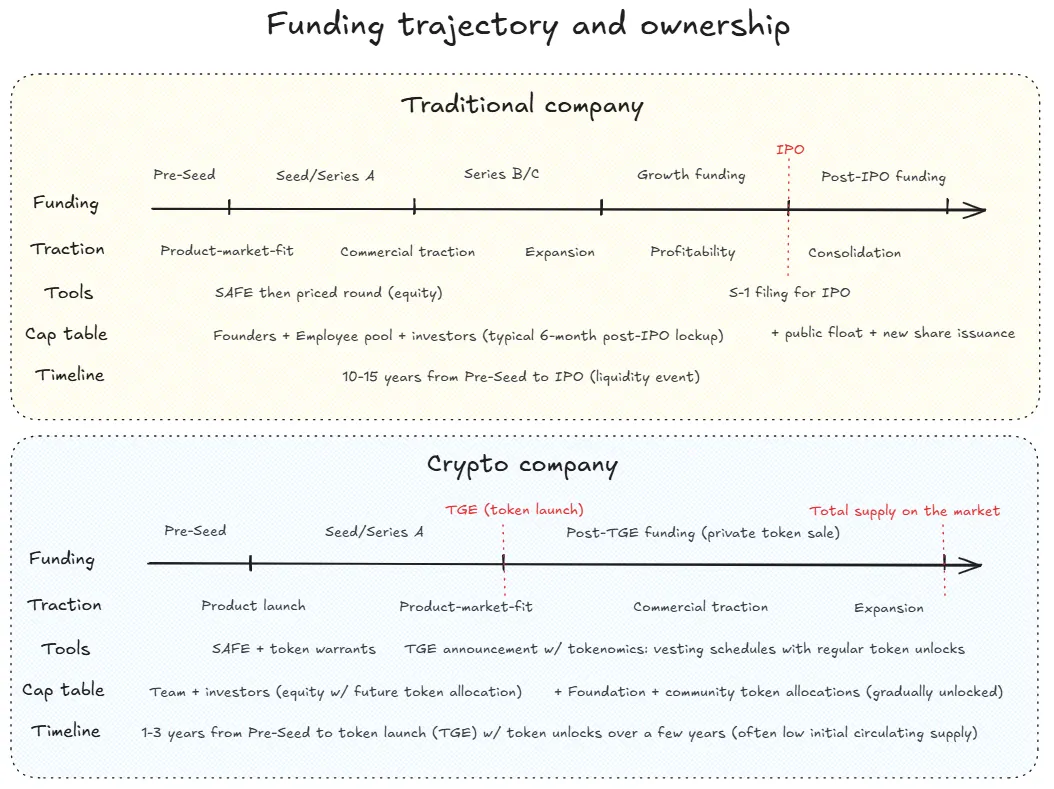

Funding trajectory & ownership

In the traditional startup world, early funding follows a well-worn path: seed round, Series A, B, and beyond, eventually leading to an IPO or acquisition. Ownership is represented by shares, and liquidity is typically delayed until a public listing often years after the initial investment.

Protocol businesses compress and reshape this trajectory. Early funding often occurs via SAFEs and token warrants, where investors commit capital in exchange for future tokens alongside equity. This opens a path to earlier liquidity (sometimes even before the protocol generates meaningful revenue) because tokens can begin trading on public markets once they launch. Post-launch, protocols may conduct additional token sales to raise funds from strategic investors, typically with vesting schedules and lockups designed to prevent immediate selling pressure. What emerges is a blended ownership model: investors hold both equity in the operating company and tokens that confer governance rights and potential economic upside. This dual structure means navigating vesting cliffs, token unlock schedules, and a different set of protections than traditional equity holders are accustomed to. It also blurs the lines between customers, contributors, and owners in ways that are unique to this asset class, which creates both opportunities and complexities for institutional investors evaluating the space.

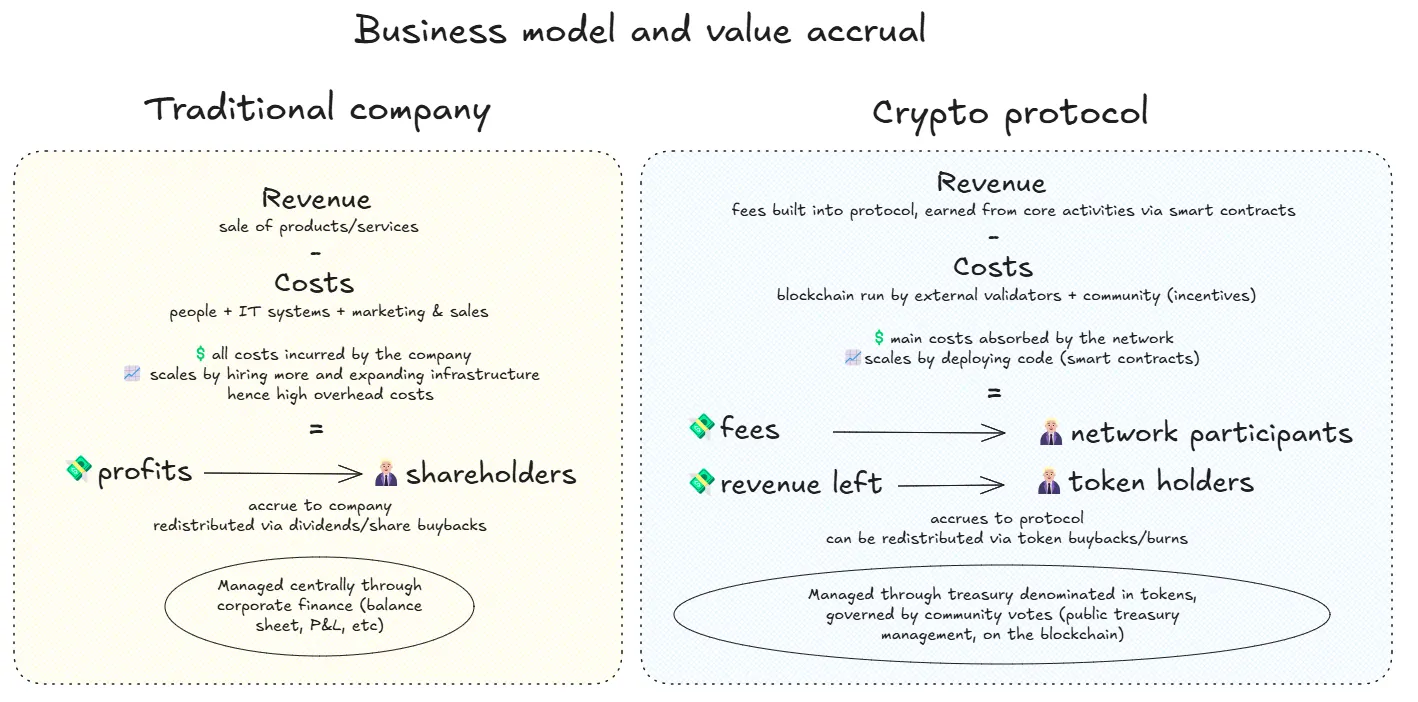

Business model & value accrual

Traditional businesses generate revenue from product sales or services, and profits are distributed to shareholders via dividends, stock buybacks, or reinvested into the business, with corporate finance managed centrally by a treasury function.

Protocol businesses embed revenue collection directly into their operations. Every time a user interacts with the protocol (whether borrowing, trading, or transferring assets depending on the protocol) a small fee is generated and either distributed to network participants or retained in a protocol-controlled treasury. Some protocols implement token buybacks, burns, or revenue-sharing mechanisms to return value to token holders, not unlike how public companies return value to shareholders through buybacks and dividends. However, token economics are more fluid than traditional corporate finance: protocols can adjust fee models, shift incentive structures, or modify revenue distribution through governance votes. And while some tokens exhibit cash-flow-like attributes, they generally lack the formal dividend rights or legal protections associated with equity. The value of holding a token comes primarily from the growth of the ecosystem it represents and the demand for participation in it, making it more akin to a growth equity investment than a yield-bearing instrument.

The spectrum: protocol businesses vs. blockchain-based businesses

It’s worth noting that not every business in the blockchain space follows the fully decentralized model described above. In practice, there is a clear spectrum. At one end sit core protocol businesses: infrastructure layers that are open-source, community-governed, and designed to be as neutral and permissionless as possible. At the other end are blockchain-based businesses: user-facing products that may use tokens for functionality or incentives but are governed more like traditional startups, with centralized teams making most decisions. Many of the most interesting projects today sit somewhere in between, combining decentralized technologies with familiar corporate structures, revenue models, and user experiences.

This distinction matters for investors. Protocol businesses tend to focus on infrastructure, security, and token-based economics, often rewarding network participants directly for their contributions. Blockchain-based businesses, on the other hand, may rely on more traditional business strategies (product-led growth, enterprise sales, recurring revenue) while leveraging blockchain to unlock new markets, streamline operations, or align their user community through token incentives. Understanding where a project sits on this spectrum is essential for evaluating both its risk profile and how value ultimately accrues.